Recent reports reveal that the U.S. government is preparing to appoint financial technology firm Robinhood as the trustee for the “Trump Account” program, which would allow millions of newborns in America to join the “retail investor headquarters” right from birth.

As background, the so-called “Trump Account” is a deferred-tax investment program established under the “Big and Beautiful” bill passed last year, which is expected to go live this July.

The bill itself only proposes a $1,000 allocation for children born between 2025 and 2028, but any child under 18 in the U.S. will be able to open an account and receive the grant. Funds provided by Congress will be required to be immediately invested in low-fee U.S. stock funds, with investments locked until the beneficiary turns 18.

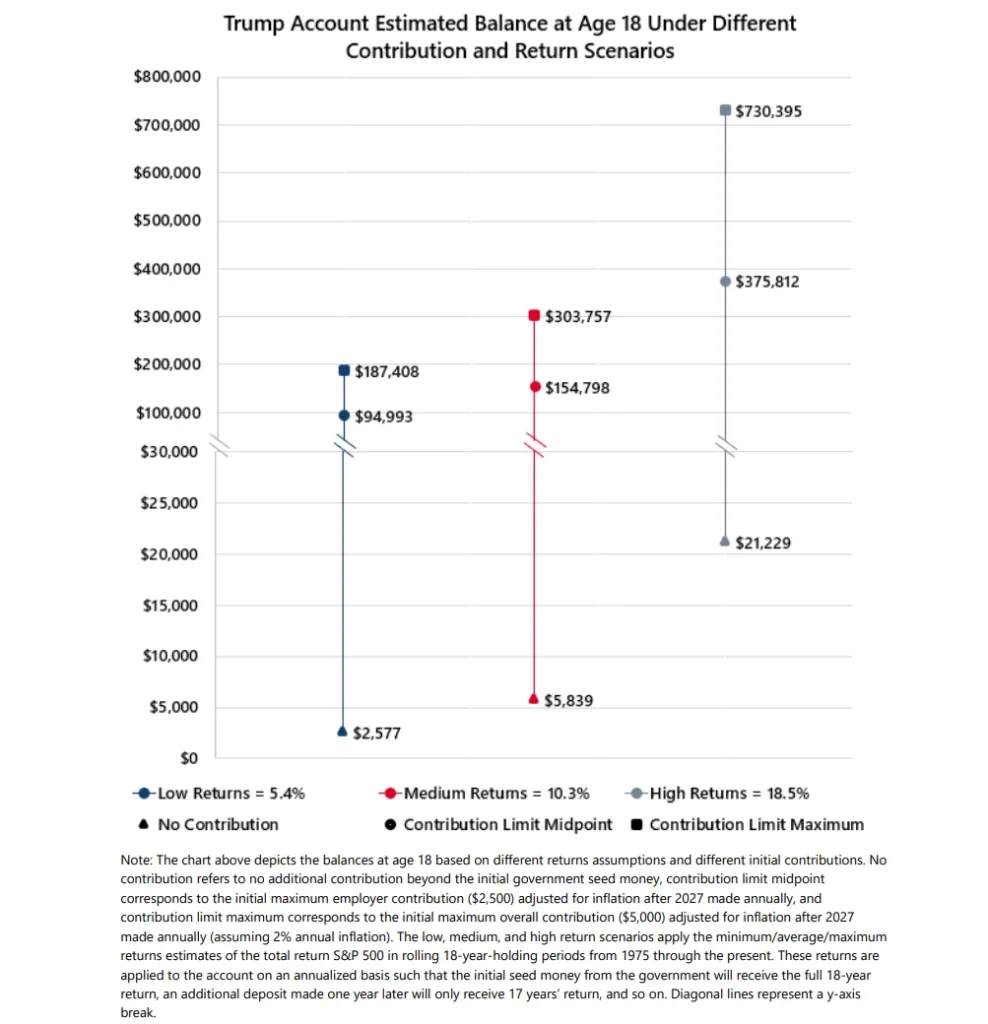

According to a forecast from the White House Economic Advisory Council last year, based on the 18-year rolling returns of the S&P 500 index from 1975 onwards, if only the $1,000 provided by the U.S. government is stored in the “Trump Account,” under a low return (annualized 5.4%) scenario, the account would grow to $2,577 by the time the baby turns 18. Under a medium return (annualized 10.3%) and high return (annualized 18.5%) scenario, the same amount would grow to $5,839 and $21,229, respectively.

Meanwhile, children who save the maximum allowed for the “Trump Account” will see their balances at age 18 reach $180,000, $300,000, and $730,000 in these three scenarios.

Robinhood Stands Out, Wall Street Giants Also Have Plans

According to Friday’s latest reports, the financial technology brokerage Robinhood, known as the “retail investor headquarters,” has begun preparations internally to become the trustee for the program. In contrast, large fund management companies like Fidelity Investments and Vanguard have not yet been included in the list of candidates and have not been consulted about the matter.

Sources say that the U.S. Department of the Treasury is expected to announce the brokerages selected for the project soon, with up to three companies likely to serve as initial trustees.

For Robinhood, a brokerage that was founded just over a decade ago and made a name for itself during the pandemic, this program could bring millions of new customers. The competition for this trustee role reportedly began last summer. Shortly after the bill was signed by Trump, Robinhood CEO Vlad Tenev publicly stated that the company was “actively engaged in this process.”

At the same time, Wall Street giants like JPMorgan (NYSE:JPM) are adopting a “wait-and-see” strategy: these banks will seek to manage the rollover accounts rather than be the first-choice institutions for managing the initial accounts. Given that many of the account holders may not even know what a “fund” is, how to handle the needs of millions of new clients will be a significant challenge. Some banks believe taking on a secondary role would be a simpler and more cost-effective way to participate.

Assets Under Management Are Expected to Keep Growing

In addition to the initial $1,000, many wealthy individuals and large corporations are adding money to these accounts.

According to unofficial statistics, Michael Dell, founder of Dell Technologies, and his wife Susan have contributed $6.25 billion to open accounts for 25 million children under the age of 10 who are not eligible for government funding, with $250 allocated to each account.

The U.S. Treasury has also launched an initiative called the “50-State Challenge,” urging wealthy individuals in each state to donate to their local “Trump Accounts.” Notable investors Ray Dalio and his wife Barbara Dalio have pledged $75 million to provide $250 for each of over 300,000 eligible children in Connecticut.

Additionally, companies like JPMorgan (NYSE:JPM), Bank of America (NYSE:BAC), Robinhood (NASDAQ:HOOD), Coinbase (NASDAQ:COIN), Broadcom (NASDAQ:AVGO), and Intel (NASDAQ:INTC) have announced their participation in this policy, injecting funds into their employees’ children’s “Trump Accounts.” According to rules released by the White House, each child’s parent’s employer can contribute up to $2,500 per year to the account