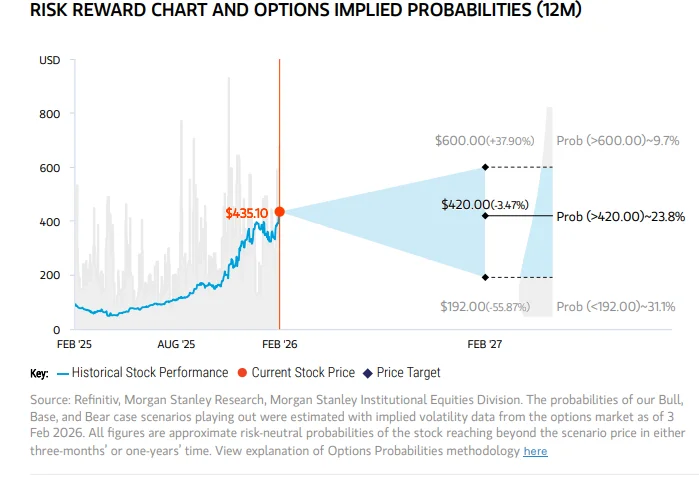

Lumentum has revealed that it has secured a multi-million-dollar CPO expansion order, expected to ship in the second half of 2027. Meanwhile, the company’s OCS business has backlog orders exceeding $400 million, with expectations to reach $100 million in quarterly revenue two quarters ahead of schedule. Morgan Stanley raised Lumentum’s target price from $350 to $420 but maintained an “Equal-weight” rating. Analysts noted that while the company’s fundamentals are strong, the stock price has already reflected the optimistic expectations of $20 per share earnings for the calendar year 2027, and the current 25x price-to-earnings valuation seems fairly priced.

Lumentum, the optical communication giant (NASDAQ:LITE), delivered a “blowout” Q2 earnings report, surpassing expectations across traditional metrics and providing solid guidance on critical AI infrastructure technologies, securing multi-million-dollar orders. The company is meeting the expectations of Wall Street bulls, though its valuation now reflects these optimistic forecasts.

In early trading today, Lumentum rose more than 10%, reaching a new all-time high.

According to Wind Trading Desk, Morgan Stanley analysts Meta A. Marshall and Mary B. Lenox released a recent report stating that Lumentum’s non-GAAP gross margin for Q2 was 42.5%, exceeding analysts’ expectation of 38.6% by 385 basis points. This was mainly due to product mix optimization and price increases on EML lasers. This performance drove earnings per share to $1.67, significantly higher than the expected $1.38.

More importantly, the company made substantial progress in the emerging CPO market. Lumentum disclosed that it has secured a multi-million-dollar CPO expansion order, which is expected to ship in the second half of 2027. Additionally, its OCS (Optical Subsystems) business backlog has surpassed $400 million, and the company expects to hit $100 million in quarterly revenue two quarters ahead of expectations.

Morgan Stanley raised Lumentum’s target price from $350 to $420, but maintained an “Equal-weight” rating. Analysts noted that while the company’s fundamentals are strong, the stock price has already priced in the optimistic expectation of about $20 earnings per share for the calendar year 2027, and the current 25x price-to-earnings multiple is already quite fully valued.

Gross Margin Exceeds Expectations, Pricing Power Evident

Lumentum’s Q2 gross margin performance became the highlight. The company reported non-GAAP revenue of $665.5 million and earnings per share of $1.67, both exceeding Morgan Stanley’s expectations of $648.6 million and $1.38.

The outperformance in gross margin was primarily driven by two factors: first, product mix improvement, with higher-margin EML lasers and OCS products gaining a larger revenue share. Second, the company successfully implemented price hikes amidst persistent supply constraints. Management indicated that despite increasing capacity by 20% in Q4, supply shortages persist, which gives the company pricing power.

Non-GAAP operating margin reached 25.2%, also significantly surpassing Morgan Stanley’s expectation of 20.6%. The company demonstrated its ability to increase both revenue and margin in a strong demand environment.

As a result, Morgan Stanley raised its earnings forecast significantly. Q3 revenue and earnings per share expectations were raised from $695.3 million and $1.56 to $804.3 million and $2.24. For FY2026, full-year revenue and earnings per share expectations were raised from $2.621 billion and $5.60 to $2.915 billion and $7.63.

CPO Business Wins Major Orders, OCS Accelerates Ramp-Up

While Lumentum’s current performance is driven by EML lasers, the company’s valuation premium is entirely based on its bets on future AI network architecture—OCS and CPO. The report reveals that progress in these two businesses is accelerating faster than expected.

CPO Secures Multi-Million-Dollar Order: Previously, the market saw CPO mostly in the technical exploration stage, but Lumentum revealed that it has received an additional “multi-million-dollar” purchase order for scale-out CPO, expected to begin shipments in the second half of 2027 (CY27). This marks a key milestone in the commercialization of CPO.

OCS Backlog Orders Surge: The optical switching business (OCS) is ramping up faster than expected. The current backlog orders exceed $400 million, and the company expects to reach a $100 million quarterly revenue scale two quarters earlier than planned. This means that the demand for optical switching in AI clusters is accelerating. The majority of the backlog orders are expected to ship in Q1 and Q2 of FY2027 (the second half of 2026).

Supply Chain Status: Ongoing Shortages, EML Controls Pricing Power

Although Lumentum increased capacity by 20% in Q4, supply shortages remain a challenge. This supply-demand imbalance has created a powerful pricing moat for the company.

The 1.6T Era Benefits EML: The company observed that the majority of initial demand for 1.6T optical modules is directed towards EML lasers. This means that in the competition for next-generation high-speed modules, EML remains dominant.

Strong Pricing Power: Management explicitly stated that due to the broad demand for laser chips, components, and subsystems, supply constraints continue, which grants the company pricing power. Morgan Stanley raised its margin expectations for the future based on the assumption that price increases will be successfully passed on to customers.

Valuation Risk: High Growth Already Priced In

Given the strong fundamentals, Morgan Stanley raised its earnings forecast significantly. Analysts predict a compound annual growth rate (CAGR) of a staggering 158% for Lumentum’s earnings from FY2025 to FY2027.

Morgan Stanley raised its target price to $420, based on a 28x P/E multiple applied to an estimated earnings per share of $15 for the calendar year 2027 (CY27).

Despite the solid fundamentals, Morgan Stanley maintains an “Equal-weight” rating. The reason is that the strong rebound in the stock price following the earnings report (up 30% from its low point) has already priced in some of the expectations.

The report points out that buy-side expectations are even more aggressive than Morgan Stanley’s, already pricing in $20 earnings per share for CY27. The current stock price corresponds to a P/E multiple of nearly 25x based on the optimistic CY27 earnings per share in Morgan Stanley’s bull case scenario.