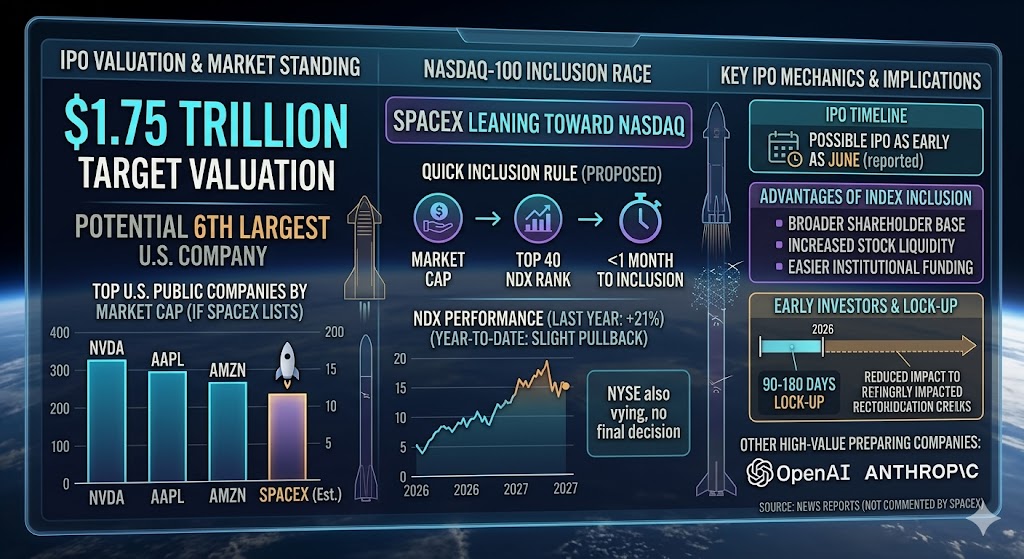

According to four sources familiar with the matter, SpaceX, the rocket and satellite company owned by Elon Musk, is inclined to list on the Nasdaq, which could become the largest IPO in history. Two of the sources indicated that SpaceX wants to be quickly included in the Nasdaq-100 Index (Nasdaq:NDX) and considers this a necessary condition for listing on the tech-heavy exchange. They also emphasized that SpaceX’s listing plans are still subject to changes.

Other sources mentioned that the New York Stock Exchange (NYSE) is also vying for the listing, but as of now, neither exchange has received a final decision from SpaceX. It was previously reported that SpaceX might launch its IPO as early as June this year.

The Nasdaq-100 Index, compiled by Nasdaq (Nasdaq:NDAQ), is regarded by large institutional investors as a benchmark for top blue-chip stocks and is a global indicator of performance for many of the world’s largest public companies, including tech giants such as (NASDAQ:NVDA), (NASDAQ:AAPL), and (NASDAQ:AMZN). The index rose about 21% last year and has seen a slight pullback so far this year.

Last month, the Nasdaq introduced a new rule that could shorten the time for large-cap companies newly listed on the exchange to be included in the Nasdaq-100 Index.

This amendment is aimed at attracting high-valued private companies like SpaceX, Anthropic, and OpenAI to list on Nasdaq. The rule has yet to be finalized and may take several months before it comes into effect.

Under the proposed “quick inclusion” rule, if a newly listed company’s market capitalization ranks within the top 40 of the Nasdaq-100’s current constituent stocks, it could be added to the index within less than a month. One source revealed that SpaceX’s IPO valuation target is about $1.75 trillion, and based on the current stock price, the company would become the sixth-largest U.S. company by market value after its listing.

Currently, newly listed companies typically have to wait up to a year before meeting the inclusion criteria for major indexes like the S&P 500 or Nasdaq-100. They must first prove their stability to attract substantial institutional investor buying.

Advantages of Index Inclusion

Being added to blue-chip indexes such as the Nasdaq-100 or S&P 500 makes it easier for companies to attract funding from large institutional investors. These institutions typically build large positions in index funds, which helps broaden the shareholder base and gradually increase stock liquidity.

While the NYSE also tracks similar indexes for the largest 100 U.S. stocks, the market’s focus is lower compared to Nasdaq, making inclusion in the Nasdaq-100 particularly important for large-cap IPOs.

For company management and early investors, stronger liquidity helps reduce the impact of large sell-offs on the stock price after the IPO lock-up period (usually 90 to 180 days). However, this does not entirely avoid the pressure on stock prices caused by large-scale insider selling.

As of the time of writing, SpaceX has not commented on the matter.

In February, it was reported that SpaceX’s advisory team had been in talks with major index providers such as Nasdaq regarding the possibility of early inclusion in core indexes.

SpaceX’s potential IPO is expected to be one of the most anticipated offerings in recent years. Currently, several well-known venture-backed companies and startups, including OpenAI and Anthropic, are also preparing for their public listings.