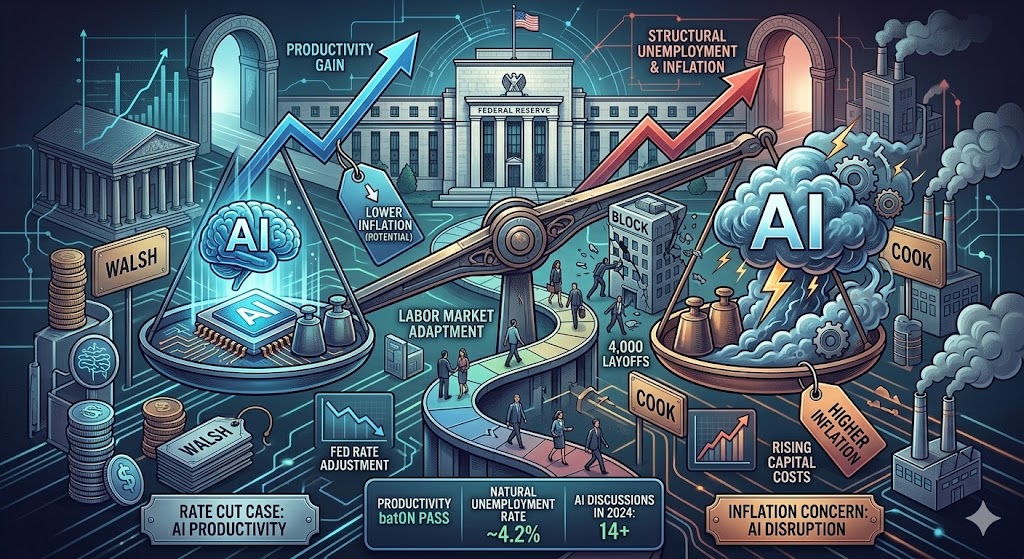

Throughout the history of the Federal Reserve, no technology has caused as much concern among policymakers as AI. Will AI create room for rate cuts, as predicted by Walsh, or, as Cook suggests, lead to structural unemployment and rising inflation?

Fed officials have generally accepted that artificial intelligence will bring about significant changes to the economy, but they are struggling to grasp the timing and extent of these changes. Internal divisions are emerging regarding AI’s potential impacts on the labor market and prices.

On Thursday, tech company Block announced it would lay off 40% of its workforce (about 4,000 employees) due to changes in employment practices driven by AI. This news highlights the current risks.

Traditionally, layoffs typically push central banks toward more accommodative monetary policies. However, the transformation caused by AI is generating different reactions. Officials suggest that rising unemployment may become a norm, with displaced workers taking longer to find new jobs. Meanwhile, rising capital returns and wage increases for those still employed will continue to exert upward pressure on inflation.

“We are in the positive, real-shock phase of the cycle, but its main manifestation is an increase in real income, rather than a significant decline in inflation,” said Adam Posen, director of the Peterson Institute for International Economics, during a discussion on inflation. He noted that the rise in stock prices has increased household wealth, while large-scale capital investment has driven up electricity and construction costs in some regions, and he expects U.S. price pressures to intensify as a result. Those who believe AI will be a deflationary force in the short term are “completely wrong,” he stated.

Is Walsh Betting on AI-Driven Rate Cuts?

This group includes Fed Chair nominee Walsh, who believes interest rates should be lowered in part to accommodate productivity gains driven by AI, thereby helping to control inflation.

Walsh, whose Senate nomination and confirmation are still pending, argued in a November 2022 Wall Street Journal column that AI is “an important inflationary force that can raise productivity and enhance U.S. competitiveness,” and that the Fed should lower interest rates to adapt to this change.

Walsh likened his position to the forward-thinking stance taken by former Fed Chairman Alan Greenspan in the mid-1990s. However, Fed policymakers are becoming increasingly cautious about this view. They are concerned about how quickly AI translates into actual labor adjustments and whether the historical principle that “new technologies replace old jobs but ultimately create more employment” still holds true.

A thought experiment published last week by Citrini Research warned of a potential “job apocalypse,” triggering a brief but significant stock market sell-off. This indicates the level of concern investors and the public have about AI. The statement by Block, which owns financial tech services Square and Cash App, seems to highlight the disruptive potential of AI: unlike past automation developments that mainly impacted blue-collar production jobs, AI may be better suited to taking over white-collar tasks such as coding or data analysis.

Programming assistants may increase employee productivity, but Block CEO Jack Dorsey stated that AI, “combined with smaller, flatter teams, is fostering a completely new way of working that will fundamentally change the way companies are built and operated. And this process is accelerating.”

An increasing body of research suggests that AI can perform various tasks, including many knowledge-based jobs that high schools, colleges, and business schools have long focused on as part of workforce “future-proofing” efforts. A 2024 paper by Brookings Institution analysts found that over 30% of U.S. workers’ job tasks could be “disrupted,” and this proportion is likely even higher today.

Fed Struggles to Keep Up

The Fed is scrambling to keep pace. A statistical review of Fed research papers and speeches by policymakers on AI, machine learning, and related topics shows that before the release of ChatGPT in late 2022, there were few such discussions. In 2023, the number increased to five, with about 17 last year, and this year, the total has already reached 14, indicating a significant acceleration.

Minutes from the Fed’s January meeting reveal that AI and productivity were thoroughly discussed, including their implications for monetary policy. At least five policymakers have spoken on the topic over the past month.

As a group, they are far from considering AI as a reason for immediate rate cuts. While they agree that productivity seems to be improving, they are reluctant to credit AI for this, preferring to attribute it to more conventional efficiency gains driven by labor shortages during the pandemic.

Even as the “productivity baton” is being passed on, policymakers seem more inclined to view AI as leading to a structurally higher unemployment rate. If interest rates are lowered to mitigate this unemployment, it could risk pushing inflation higher.

The Fed’s framework is underpinned by a long-term “natural” unemployment rate, currently thought to be around 4.2%. If unemployment falls below this level, inflationary pressures tend to accumulate.

“If AI continues to improve productivity, economic growth could remain strong, even if severe disruptions in the labor market lead to higher unemployment rates,” said Fed Governor Cook last month. “During such productivity booms, rising unemployment may not necessarily mean a surplus of idle labor. Therefore, our conventional demand-side monetary policies may not be able to alleviate AI-driven unemployment without increasing inflationary pressures.” This view has been echoed by several of his colleagues.

The issue is far from settled.

Krishna Guha, Vice Chairman of Evercore ISI, argued that the loss of workers’ bargaining power could be a reason for a lower natural unemployment rate. As employees become more willing to keep their jobs and accept lower wage increases, downward pressure on inflation could occur. This argument aligns with Walsh’s conclusion on rate cuts, though for different reasons.

However, Fed officials’ public statements paint a more complicated picture: some workers are facing job pressures, others are gaining new productive potential, wealth growth is driving consumption in some households, resource constraints during the AI build-out, and high expected investment returns may push up the base interest rate.

“There are all sorts of predictions about AI’s rollout, effectiveness, energy efficiency, and its effects on the labor market,” said Richmond Fed President Barkin last week. “The only thing that’s certain is that these predictions will certainly be wrong. Whether overly optimistic or overly pessimistic, you can only figure it out as you go along.”