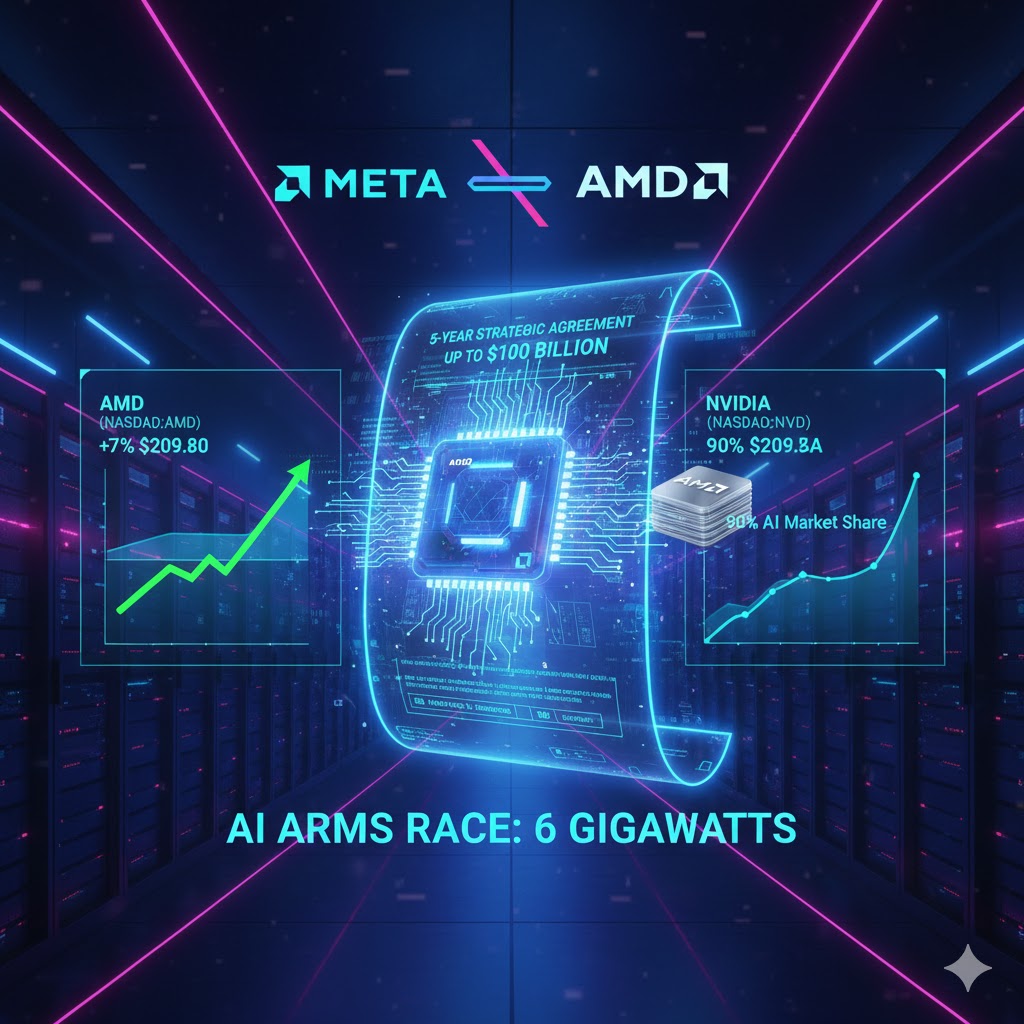

Meta has reached a groundbreaking five-year strategic agreement with AMD (NASDAQ:AMD), valued at up to $100 billion, to procure 6 gigawatts of computing power chips and deeply customize the MI450 processor. As part of the deal, Meta will receive warrants to purchase up to 160 million shares of AMD, potentially owning up to 10% of the company.

This move aims to secure computing power supply through equity bundling and reduce reliance on Nvidia, marking a new phase in the AI arms race where tech giants are accelerating the global competition by deep customization and reshaping their supply chains.

Meta Platforms (NASDAQ:META) and AMD (NASDAQ:AMD) have finalized a massive, unprecedented five-year deal to purchase AI chips and data center equipment, valued at up to $100 billion. This collaboration signals an escalation in the AI infrastructure investment race among global tech giants, while also providing AMD with a key strategic foothold in the computing power market traditionally dominated by Nvidia.

According to the latest disclosed agreement, Meta Platforms (NASDAQ:META) will purchase up to 6 gigawatts of AMD (NASDAQ:AMD) processors and data center equipment over the next five years. Reports from Reuters and The Wall Street Journal estimate the total value of the deal to be between $60 billion and over $100 billion. The first batch of devices, featuring the new MI450 graphics processing unit (GPU) from AMD, is set to begin deployment in the second half of this year.

As part of an innovative financial arrangement, Meta Platforms (NASDAQ:META) will receive warrants to buy up to 160 million shares of AMD (NASDAQ:AMD) at a price of $0.01 per share. If specific technical and business milestones are met and AMD’s stock price reaches $600 in the future, Meta could potentially acquire around 10% of AMD, becoming one of its core shareholders.

The announcement quickly triggered a strong market reaction, with AMD (NASDAQ:AMD) shares rising nearly 7% in early trading, reaching $209.80. This deal not only boosts AMD’s revenue prospects but also highlights how large tech companies are reshaping industry supply chains through equity-linked partnerships to secure AI computing power.

Deep Customization and Accelerated Computing Power Deployment

At the heart of this partnership is a highly customized hardware solution. AMD (NASDAQ:AMD) will provide Meta Platforms (NASDAQ:META) with a range of products, including customized central processing units (CPUs), optimized for Meta’s low-power, high-performance needs.

According to Bloomberg, AMD CEO Lisa Su stated that the company is providing “high-performance, energy-efficient infrastructure optimized for Meta’s workloads,” and noted that Meta assisted in the design of the MI450 chip. This chip is primarily optimized for the “inference” phase of AI (the process by which AI models respond to user queries). The Wall Street Journal pointed out that the MI450 uses a “chiplet” architecture design, which makes it easier to customize compared to traditional monolithic silicon chips.

“We have very ambitious goals,” said Santosh Janardhan, Meta’s global infrastructure head, in an interview. “Being able to define the required technical specifications more tightly was one of the key reasons why Meta and AMD formed this deep partnership.”

Challenging Nvidia’s Market Dominance

This deal holds significant strategic importance for AMD (NASDAQ:AMD). Currently, Nvidia (NASDAQ:NVDA) controls approximately 90% of the global AI chip market, with a market value of $4.66 trillion, while AMD’s market cap is around $320 billion.

Just last week, Meta pledged to purchase millions of Nvidia processors to fuel its AI expansion. However, to reduce supply chain risks and enhance bargaining power, tech giants are actively seeking reliable “second suppliers.” Ben Bajarin, a chip analyst at Creative Strategies, pointed out:

“Meta is in a unique position to control the entire tech stack—they can use anyone’s computing power. This deal also underscores the current limitations in the computing power industry.”

Santosh Janardhan added that given Meta’s massive need for data centers and infrastructure, multiple chip suppliers and technological paths are required. He emphasized that Meta will continue to procure chips from Nvidia while also advancing its in-house AI chip development projects.

Equity Bundling and High Capital Expenditures

The structure of Meta’s acquisition of AMD (NASDAQ:AMD) stock warrants has drawn attention to financing models in the AI industry. Last October, OpenAI also reached a very similar agreement with AMD (NASDAQ:AMD). This model, known as “circular financing,” involves customers securing equity or investment commitments from suppliers through large procurement orders. It is increasingly becoming a common method for AI giants to lock in key technologies.

This partnership also reflects the massive capital expenditure pressures facing tech giants in the AI era. Meta Platforms (NASDAQ:META) CEO Mark Zuckerberg has previously identified AI as the company’s top priority, announcing ambitious plans to build “tens of gigawatts” or even “hundreds of gigawatts” of computing power. According to Meta’s earnings report released last month, the company’s capital expenditures for 2026 could reach up to $135 billion, with plans to build around 30 data centers in the U.S. and globally to keep up with the intense global AI race and compete with companies like OpenAI.

Lisa Su remarked that the Meta-AMD partnership is “moving to the next level.” For AMD, which achieved $34.6 billion in revenue last year, even an additional $10 billion in annual sales would significantly accelerate its race to catch up with Nvidia (NASDAQ:NVDA) in the AI chip market.