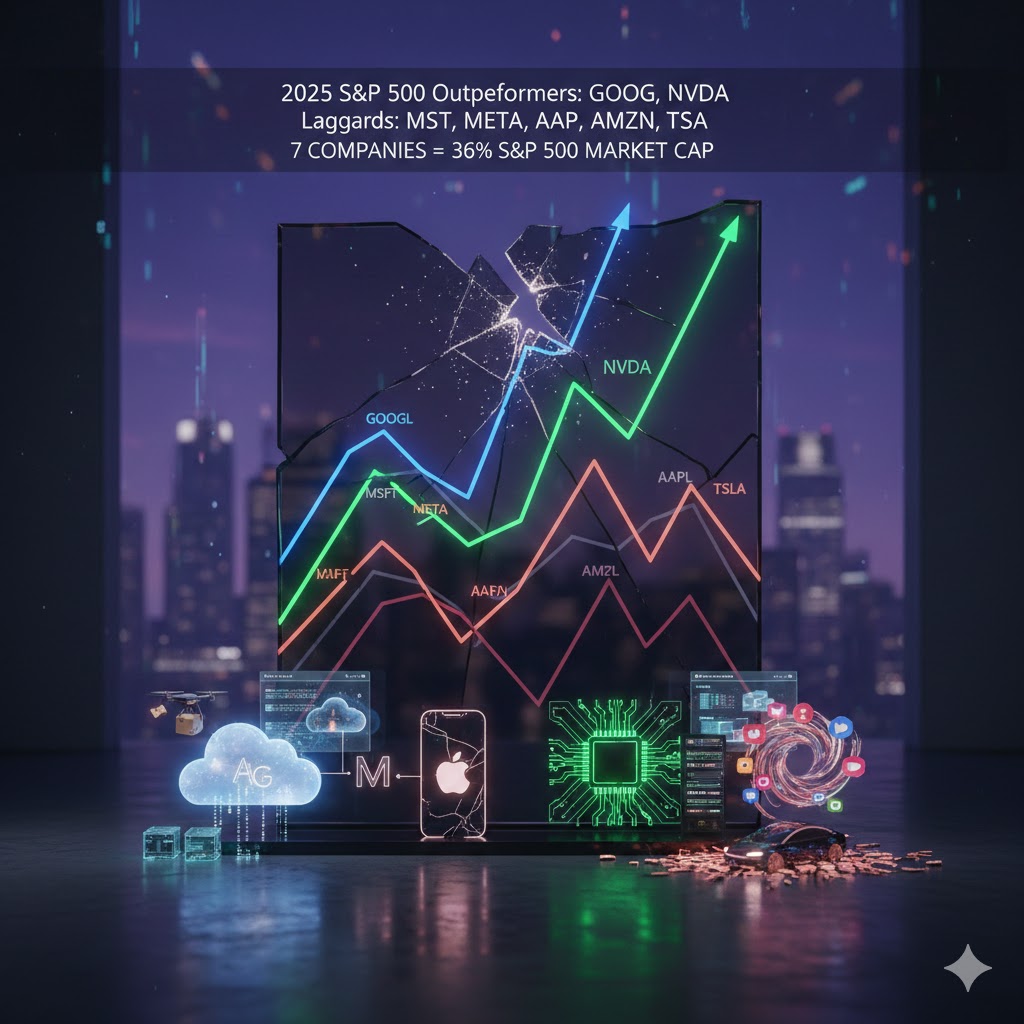

The “Magnificent Seven” tech stocks, which once propelled the U.S. stock market to consecutive record highs, are increasingly moving in different directions. As investors grow more cautious regarding the Artificial Intelligence spending boom, the performance of this mega-cap portfolio has shown significant disparity over the past year.

Data from The Wall Street Journal reveals that in 2025, only Alphabet (GOOG) and Nvidia (NVDA) outperformed the S&P 500. The remaining five giants—Microsoft (MSFT), Meta Platforms (META), Apple (AAPL), Amazon (AMZN), and Tesla (TSLA)—all lagged behind the broader market. Fund managers note that this group is no longer synonymous with market leadership. David Bahnsen, Chief Investment Officer at The Bahnsen Group, stated:

“The correlation between them has collapsed. Today, the only thing they have in common is the trillion-dollar market cap label.”

This shift marks a new phase in the AI trade logic since the start of this bull market, as investors become more selective. Some capital is rotating toward sectors like healthcare, expecting AI dividends to spread, while others are focusing on chipmakers or energy companies. This reflects a market transition from general AI themes toward specific sub-sectors and tangible profitability.

The AI Arms Race Intensifies Internal Divergence

The AI spending frenzy is creating a structural divide within the “Magnificent Seven.” Amazon, Alphabet, Microsoft, and Meta have explicitly pivoted to become “Hyperscalers,” investing hundreds of billions of dollars to train new AI models, build data centers, and expand cloud computing infrastructure. Meanwhile, Nvidia continues to dominate the high-end AI chip market, providing the core computational power for the most advanced AI models.

In contrast, other members are falling behind. Apple’s stock underperformed the S&P 500 last year, as the iPhone maker faced market criticism for its cautious AI investment and slower progress relative to competitors. Tesla, once the market’s primary focus, has seen its stock performance significantly trail most of its peers as growth in electric vehicle sales slows down.

Michael Arone, Chief Investment Strategist at State Street Global Advisors, pointed out:

“They are at different stages of development. Previously, the rising tide lifted all boats; now, we are going to see clear winners and losers.”

Individual Investors Shift Their Focus

Individual investors, who were long-time stalwarts of the “Magnificent Seven,” are gradually turning their attention to other market segments. According to data from Vanda Research, the proportion of retail trading in these seven stocks last year was significantly lower than the levels seen in 2023 and 2024.

Taking Tesla as an example—a long-time favorite among retail traders—the decline in trading activity is particularly stark. In 2025, the average daily retail trading volume for the stock dropped by approximately 43% compared to its peak two years prior. Despite this divergence, these seven companies still wield massive influence over the market. According to Dow Jones Market Data, they collectively account for about 36% of the S&P 500’s total market capitalization, meaning their movements will continue to dictate the performance of the broader market.