The “Magnificent Seven” tech stocks, which once propelled the U.S. stock market to consecutive record highs, are increasingly moving in different directions. As investors grow more cautious regarding the Artificial Intelligence spending boom, the performance of this mega-cap portfolio has shown significant disparity over the past year.

Data from The Wall Street Journal reveals that in 2025, only Alphabet (GOOG) and Nvidia (NVDA) outperformed the S&P 500. The remaining five giants—Microsoft (MSFT), Meta Platforms (META), Apple (AAPL), Amazon (AMZN), and Tesla (TSLA)—all lagged behind the broader market. Fund managers note that this group is no longer synonymous with market leadership. David Bahnsen, Chief Investment Officer at The Bahnsen Group, stated:

“The correlation between them has collapsed. Today, the only thing they have in common is the trillion-dollar market cap label.”

This shift marks a new phase in the AI trade logic since the start of this bull market, as investors become more selective. Some capital is rotating toward sectors like healthcare, expecting AI dividends to spread, while others are focusing on chipmakers or energy companies. This reflects a market transition from general AI themes toward specific sub-sectors and tangible profitability.

The AI Arms Race Intensifies Internal Divergence

The AI spending frenzy is creating a structural divide within the “Magnificent Seven.” Amazon, Alphabet, Microsoft, and Meta have explicitly pivoted to become “Hyperscalers,” investing hundreds of billions of dollars to train new AI models, build data centers, and expand cloud computing infrastructure. Meanwhile, Nvidia continues to dominate the high-end AI chip market, providing the core computational power for the most advanced AI models.

In contrast, other members are falling behind. Apple’s stock underperformed the S&P 500 last year, as the iPhone maker faced market criticism for its cautious AI investment and slower progress relative to competitors. Tesla, once the market’s primary focus, has seen its stock performance significantly trail most of its peers as growth in electric vehicle sales slows down.

Michael Arone, Chief Investment Strategist at State Street Global Advisors, pointed out:

“They are at different stages of development. Previously, the rising tide lifted all boats; now, we are going to see clear winners and losers.”

Individual Investors Shift Their Focus

Individual investors, who were long-time stalwarts of the “Magnificent Seven,” are gradually turning their attention to other market segments. According to data from Vanda Research, the proportion of retail trading in these seven stocks last year was significantly lower than the levels seen in 2023 and 2024.

Taking Tesla as an example—a long-time favorite among retail traders—the decline in trading activity is particularly stark. In 2025, the average daily retail trading volume for the stock dropped by approximately 43% compared to its peak two years prior. Despite this divergence, these seven companies still wield massive influence over the market. According to Dow Jones Market Data, they collectively account for about 36% of the S&P 500’s total market capitalization, meaning their movements will continue to dictate the performance of the broader market.

In recent years, many investors followed a simple recipe to beat the market: heavy concentration in U.S. mega-cap tech stocks.

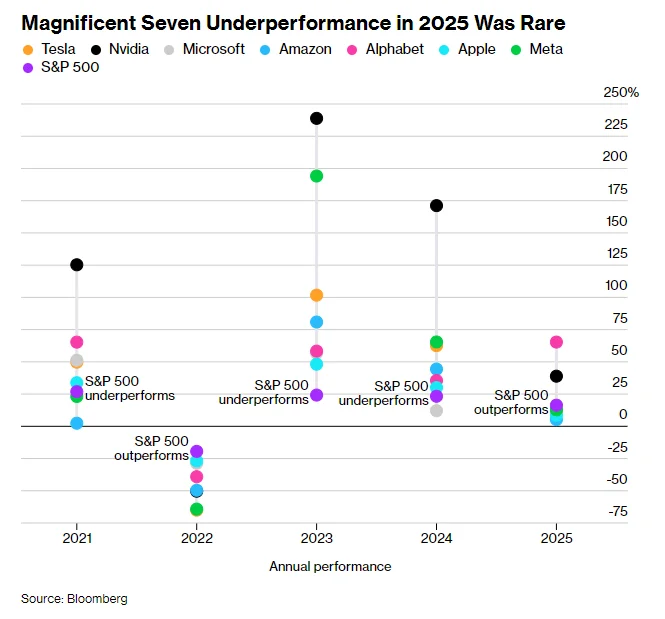

While this strategy yielded handsome rewards for a long time, it lost its luster in 2025. For the first time since the Federal Reserve began its rate-hiking cycle in 2022, the majority of the “Big Tech” firms underperformed the S&P 500 (SPX). Although an index tracking the “Magnificent Seven” rose 25% in 2025—outpacing the S&P 500’s 16%—this gain relied entirely on the explosive performance of Alphabet (GOOGL) and Nvidia (NVDA).

Many Wall Street professionals expect this divergence to persist through 2026 as earnings growth for tech giants slows and skepticism grows regarding the returns on massive Artificial Intelligence (AI) investments. Early 2026 data supports this view: the Magnificent Seven index is up only 0.5%, while the S&P 500 has climbed 1.8%. In this environment, selective stock picking within the group has become critical.

“The market is no longer a ‘one-size-fits-all’ trade,” said Jack Janasiewicz, Lead Portfolio Strategist at Natixis Investment Managers Solutions, which manages $1.4 trillion. “If you just blindly buy the whole basket, the laggards are likely to cancel out the winners.”

Cooling Enthusiasm and Narrowing Growth Gaps

This three-year bull market has been spearheaded by tech titans. Since the bull run began in October 2022, just four companies—Nvidia, Alphabet, Microsoft (MSFT), and Apple (AAPL)—have accounted for over one-third of the S&P 500’s total gains. However, as capital begins to rotate into other S&P 500 constituents, enthusiasm for Big Tech is cooling.

With earnings growth slowing, investors are no longer satisfied with the “AI will make us rich” narrative; they want tangible financial results. Data indicates that earnings growth for the Magnificent Seven is projected to be around 18% in 2026—the slowest since 2022. This narrows their lead significantly over the other 493 S&P 500 companies, which are expected to see a 13% increase.

“We are seeing the breadth of corporate earnings growth expanding, and that trend will continue,” noted David Lefkowitz, Head of U.S. Equities at UBS Global Wealth Management. “Tech is no longer the only game in town.”

One silver lining for the group is that valuations have moderated. The Magnificent Seven index currently trades at 29 times forward earnings, well below the highs of over 40 times seen at the start of the decade. By comparison, the S&P 500 trades at 22 times, and the Nasdaq 100 at 25 times.

Outlook for the Magnificent Seven in 2026:

Nvidia

The dominant AI chipmaker is under pressure from rising competition and concerns over the sustainability of capital expenditure from its largest customers. While the stock has soared roughly 1,100% since late 2022, it has retreated 8% since hitting an all-time high on October 29 last year.

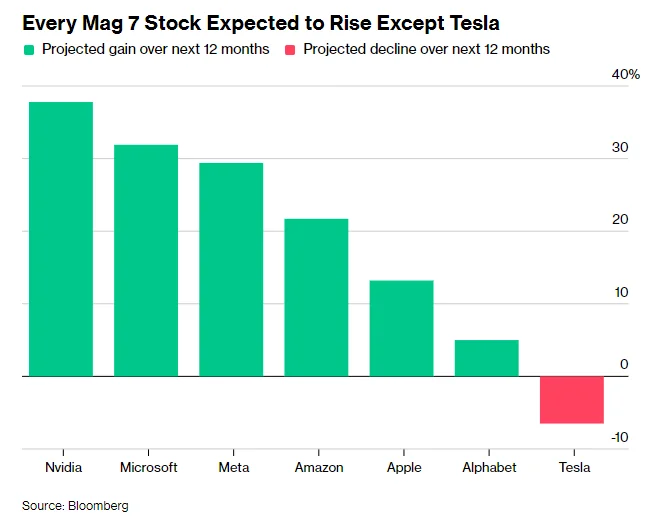

Rival AMD (AMD) has secured data center chip orders from OpenAI and Oracle (ORCL), while major customers like Google are accelerating the deployment of in-house custom chips. Nevertheless, Nvidia’s revenue continues to grow rapidly as chip demand still outstrips supply. Wall Street remains bullish: 76 out of 82 analysts rate it a “Buy,” with an average price target implying 39% upside—the highest among the Seven.

Microsoft

2025 marked the second consecutive year Microsoft underperformed the S&P 500. As a major spender in the AI race, Microsoft is expected to see capital expenditures approach $100 billion for the fiscal year ending June 2026, with analysts predicting a further climb to $116 billion the following year.

While data center expansion has boosted cloud revenue growth, the company has struggled to convince customers to pay significantly more for AI-integrated software. Brian Mulberry, Client Portfolio Manager at Zacks Investment Management, notes that investors are waiting for these massive investments to translate into real bottom-line results.

Apple

Apple took the most conservative approach to AI among the group, a strategy that weighed on its stock in early 2025, with shares falling nearly 20% by August. However, Apple subsequently became an “Anti-AI play,” attracting investors wary of high-cost AI risks, and surged 34% by the end of 2025. Strong iPhone sales have reassured investors that core demand remains robust.

The key for 2026 is accelerating growth. While the company narrowly avoided its longest losing streak since 1991 last week, momentum has slowed. Markets expect revenue to grow 9% in the fiscal year ending September 2026—the fastest since 2021. With a forward P/E of 31x (second only to Tesla), Apple’s performance must dazzle to sustain its valuation.

Alphabet (Google)

A year ago, investors feared Google was falling behind OpenAI. Today, Google is a consensus “darling,” leading the AI field on multiple fronts. Its Gemini AI model has received widespread acclaim, and its in-house TPUs are seen as a major revenue driver that could even challenge Nvidia’s dominance.

In 2025, Google was the best performer of the Seven, rising over 65%. However, with its market cap nearing $4 trillion and a P/E of 28x (well above its five-year average of 20x), analysts expect more modest gains of about 3.9% in 2026.

Amazon

After seven consecutive years as the laggard of the group, Amazon (AMZN) has staged a strong comeback in early 2026. Optimism centers on its cloud business, AWS, which recently posted its fastest growth in years. Investors expect efficiency gains from warehouse automation and robotics to pay off soon. Clayton Allison, Portfolio Manager at Prime Capital Financial, believes the market has yet to fully price in this value, drawing parallels to Google’s turnaround last year.

Meta

Meta Platforms (META.) most clearly reflects investor skepticism regarding “AI overspending.” CEO Mark Zuckerberg has spent billions on acquisitions and talent, including a $14 billion investment in Scale AI. However, after Meta raised its 2025 capex to $72 billion and forecasted “significantly higher” spending for 2026, the stock tumbled. Since its August 2025 high, the stock has dropped 17%. Meta’s primary task in 2026 is proving these investments drive profit growth.

Tesla

Tesla (TSLA) flipped from laggard to leader in the second half of 2025 as Elon Musk pivoted focus from lackluster EV sales to autonomous vehicles and robotics, sending shares up over 40%. This rally pushed Tesla’s forward P/E to a staggering 200x. While revenue is expected to return to 12% growth in 2026 after a stagnant period, Wall Street analysts remain pessimistic about the stock price, with an average target predicting a 9.1% decline over the next 12 months.

On Monday, $Amazon (AMZN)$ officially launched a dedicated website for Alexa+, Alexa.com, allowing select users to interact with the assistant via a web browser. This move signals a more direct competition between Amazon and OpenAI’s flagship product, ChatGPT.

The Alexa.com website is currently accessible only to Alexa+ users. As a next-generation AI assistant launched by Amazon last February, Alexa+ is still in its early preview phase. To gain access, users must either join a waitlist or purchase newer compatible devices.

Amazon stated that through Alexa.com, consumers can “get quick answers, dive deep into complex topics, create content, plan travel itineraries, and receive assistance with homework.” The company also noted that users can manage their smart home devices directly within the Alexa+ chat window.

Amazon’s primary motivation for launching a web-based version of Alexa is to ensure that users can interact with the AI assistant seamlessly across different terminal interfaces. Previously, Alexa+ was only accessible via mobile applications or select Amazon Echo smart speakers.

Furthermore, the launch of this website brings Amazon’s service closer to the usage models of other popular AI chatbots. Competitors like OpenAI, Google, Anthropic, and Perplexity all primarily support direct user access through web browsers.

With the successful deployment of generative AI products like ChatGPT and Google Gemini, Amazon has faced increasing pressure to upgrade its hardware and software ecosystems to keep pace with the current technological wave.

Since its launch last year, Alexa+ has been gradually rolled out to the public. Amazon revealed that over one million users currently have access to the service.

In fact, when Amazon first announced Alexa+ last year, it teased the upcoming launch of the Alexa.com website, stating it would go live within months. In July of the same year, the company told The Washington Post that the feature would be available to early preview users during the summer.