Tesla’s(TSLA) current high valuation relies heavily on the visionary potential of its Robotaxi and Full Self-Driving (FSD) technology. Based on the latest operational updates and product roadmaps, the core investment logic is summarized below:

Robotaxi Status: Competitive Pricing and Expanding Range, but Scale Remains Limited

More Affordable than Waymo According to DriveTesla and Robotracker, Tesla’s Robotaxi initially launched with a flat fare of $4.20 per trip, later adjusting to $6.90 as coverage expanded. The service has now largely transitioned to dynamic pricing, averaging approximately $1.50 per mile. In comparison, Waymo’s pricing in San Francisco and Phoenix averages around $2.50 per mile—rising above $3.00 during peak hours—giving Tesla a clear price advantage.

Steady Geographic Expansion While currently only operational in two core hubs—Austin, Texas, and the San Francisco Bay Area—Tesla’s coverage area already exceeds that of Waymo. By 2026, the company plans to expand to multiple states, with a confirmed list of cities including Miami, Las Vegas, Houston, and Dallas.

Key Bottlenecks Persist The primary challenge remains fleet size, which leads to prolonged wait times. As of December 2025, approximately 1,655 Robotaxis were registered in California, but only 132 were in active operation; Austin’s fleet stood at just 40 vehicles. Consequently, Robotaxi has yet to contribute significant revenue and remains in the early stages of commercial validation.

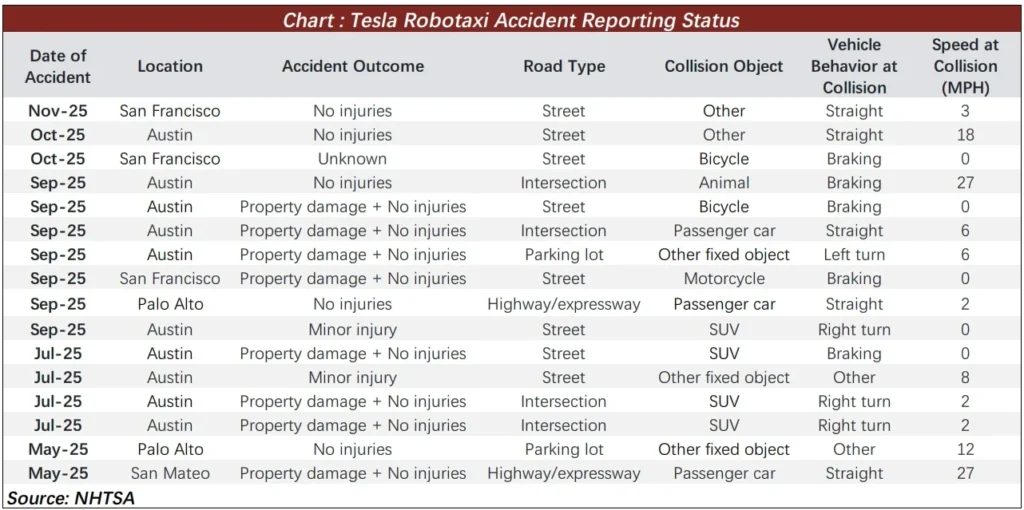

Robust Safety Performance The safety record has been stable since launch with no severe accidents reported. Of the 16 incidents reported to the NHTSA (National Highway Traffic Safety Administration) since May 2025, only two involved airbag deployment—both caused by other vehicles. Tesla’s vehicles sustained no structural damage in these cases, and the majority of incidents resulted in no injuries, indicating a high level of overall safety.

FSD: Rising Penetration and “Grok” Integration—China as the Critical Variable

While Robotaxi may not drive significant revenue in the short term, it serves as a powerful catalyst for FSD adoption:

Technical Iteration and Surging Subscription Rates FSD V14 utilizes a unified system compatible with both consumer vehicles and Robotaxis, with only minor functional differences (e.g., consumer cars retain Autopark, which is unnecessary for Robotaxis). V14 features more conservative driving logic and, following an architectural upgrade, may integrate a streamlined version of the Grok AI system, which is expected to further increase MPI (Miles Per Intervention).

The FSD subscription “take rate” has surged from single digits to between 13% and 19% as of September 2025. By the end of 2025, with Tesla’s cumulative production reaching approximately 9 million vehicles, the estimated number of FSD subscribers sits around 1 million. Since subscribers are concentrated in the U.S. (which accounts for roughly 50% of Tesla’s recent sales), the U.S. penetration rate likely exceeds 20%.

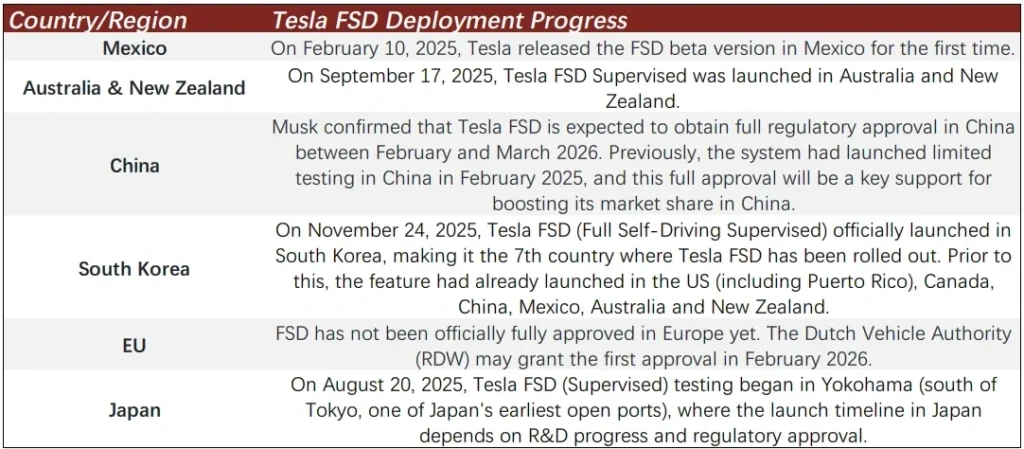

2026 Global Acceleration: Focus on the China Market Following the Grok integration and subsequent performance boosts, the market expects the launch of “unsupervised” Robotaxi operations and a driverless version of FSD. By 2026, commercialization is expected to move into Europe, Southeast Asia, and other regions.

As Tesla’s second-largest market, China remains a crucial growth lever. Currently, FSD is limited to a one-time purchase of 64,000 RMB (~$9,000) with a penetration rate under 5%. If full regulatory approval is granted and Tesla switches to a monthly subscription model, the lower entry barrier is expected to significantly drive adoption in the region.

Cybercab: Mass Production Slated for 2026 with a 2-Million Unit Target

Tesla has already begun testing the Cybercab production system. Elon Musk previously indicated that mass production is scheduled to begin in April 2026. Multiple Cybercab prototypes have been spotted during road tests in Austin. Notably, these test vehicles are equipped with temporary steering wheels and mirrors to satisfy current safety and regulatory requirements.

Tesla envisions the Cybercab as the “highest-volume vehicle in history,” targeting an annual capacity of 2 million units. However, given the realities of automotive manufacturing, achieving this goal in the short term remains a formidable challenge.

Summary: 2026—The Year of Scalability and Execution

Compared to the expectations set in early 2025, many of Tesla’s Robotaxi milestones have already been achieved: accident rates are low, and an unsupervised version is in testing. The core watchpoints for the future are twofold:

- Fleet Scaling: Current wait times of 30–40 minutes and the continued need for human supervision mean the service is not yet “fully commercialized.”

- Cybercab Production: The pace of the production ramp-up will directly determine whether Tesla’s valuation logic can be realized.