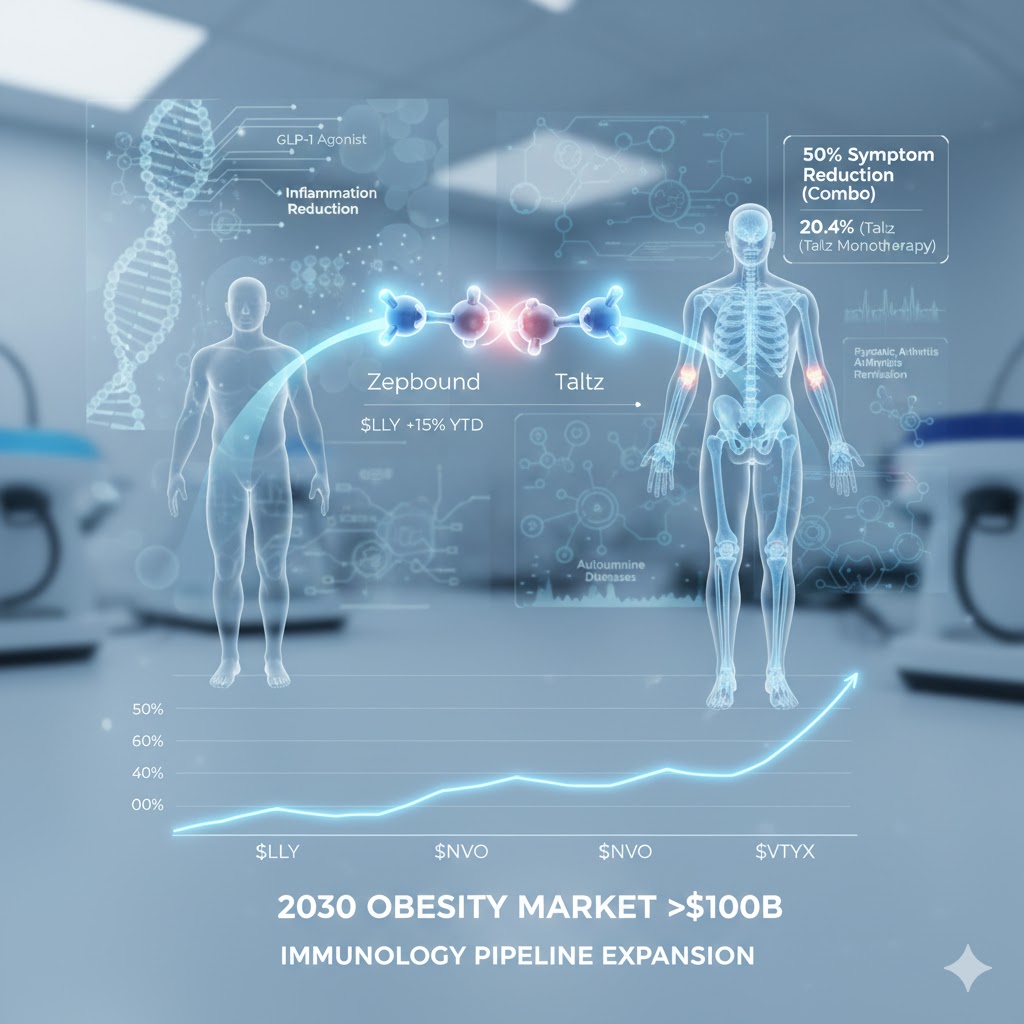

A latest study from Eli Lilly (LLY) reveals that combining its popular weight-loss injection, Zepbound, with the arthritis drug Taltz, is significantly more effective at relieving joint pain and swelling than using either drug alone. This Lilly-backed research opens a new frontier for the application of GLP-1 medications in inflammatory and autoimmune diseases.

Key Study Findings

The study enrolled 271 patients suffering from both obesity and active psoriatic arthritis. Results showed that the combination therapy outperformed Taltz monotherapy in helping patients lose weight and manage arthritis symptoms, meeting the trial’s primary objectives. According to a statement from Eli Lilly, approximately one-third of patients on the combination therapy saw their psoriatic arthritis symptoms reduced by at least half, compared to 20.4% of those using only Taltz.

GLP-1 receptor agonists like Zepbound have already been proven to lower inflammation levels in patients with diabetes and obesity. While observational studies and case reports have previously linked them to improvements in autoimmune conditions such as psoriasis, this study provides the first clinical validation of that theory.

Broadening the Scope of Treatment

With the obesity drug market projected to reach $100 billion by 2030, part of Zepbound’s appeal lies in its potential to address other health complications, including sleep apnea and heart failure. Eli Lilly has integrated this cross-disciplinary approach into the development of its next-generation weight-loss drug, retatrutide, which is currently being studied for conditions such as knee osteoarthritis and chronic kidney disease.

Eli Lilly stated it plans to discuss the study results with regulatory agencies, a move that could lead to expanded label indications or modified clinical treatment recommendations. In the United States, approximately 65% of adults with psoriatic arthritis are also obese, meaning the majority of these patients already qualify for Zepbound treatment.

Strategic Growth and Acquisitions

The Indianapolis-based pharmaceutical giant is also exploring the efficacy of the Zepbound-Taltz combination for plaque psoriasis and inflammatory bowel disease. Results for the plaque psoriasis trial are expected to be released in the first half of this year.

Taltz is one of several Eli Lilly drugs treating inflammatory conditions, with annual sales exceeding $3 billion; however, its key patent protections are set to expire in the coming years. This combination research is a core component of Lilly’s strategy to leverage its success in obesity to drive growth in other sectors like immunology.

Furthermore, the company is actively pursuing deals to bolster its pipeline. On Wednesday, Eli Lilly announced it would acquire Ventyx Biosciences ($VTYX.US) for up to $1.2 billion, gaining access to oral therapies for inflammatory diseases. This acquisition builds on earlier deals for companies like Morphic Therapeutic and Dice Therapeutics, which specialize in oral autoimmune treatments.