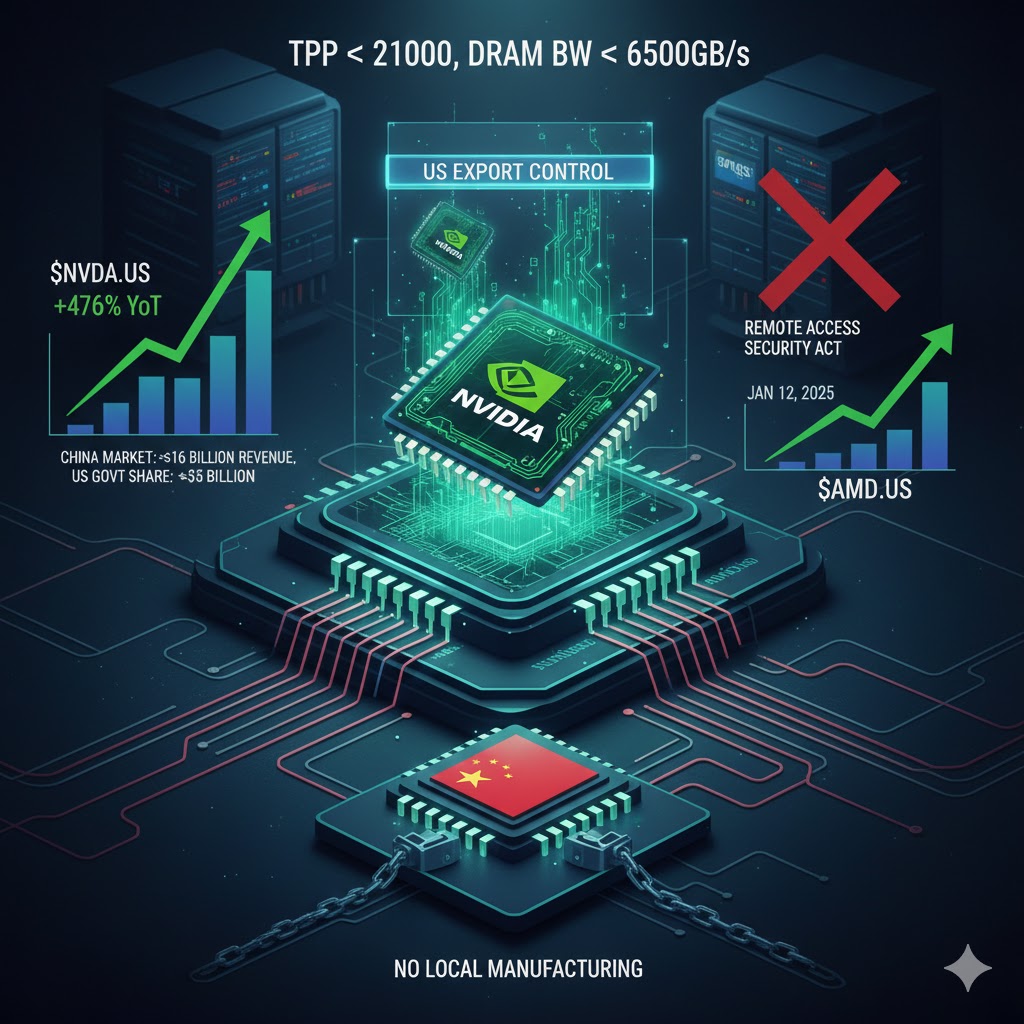

The United States has once again legally eased export controls on the sale of Nvidia’s H200 chips to China.

On January 14, the Bureau of Industry and Security (BIS), under the U.S. Department of Commerce, amended its export control regulations to relax restrictions on high-performance chips. The new thresholds allow for the export of chips with a Total Processing Performance (TPP) of less than 21,000 and a total DRAM bandwidth of less than 6,500 GB/s. This adjustment effectively creates a legal pathway for products such as Nvidia (NVDA) H200 and AMD MI325X to be exported.

A veteran researcher of technology policy noted that this adjustment constitutes a formal rule change, providing a clear legal basis for future transactions.

The revision of these regulatory details is tied to the U.S. government’s official announcement regarding the issuance of export licenses for the H200 and MI325X to mainland China. Because previous regulations—specifically the “October 7 Rule” of 2022 and the “October 17 Rule” of 2023—imposed strict limits on TPP and memory bandwidth, the act of granting new licenses would have conflicted with existing standards without these formal amendments.

“It isn’t as simple as saying ‘you can sell now’ and sales begin immediately; following formal legal procedures takes time,” explained another tech policy researcher. “Simply approving licenses without updating the export control regulations would have been inconsistent with the regulatory framework.”

New Standards and Restrictive Conditions

Records show that the “October 17 Rule” of 2023 required licenses for any chip export to mainland China or Macau that met specific criteria ($TPP \ge 4,800$, or $TPP \ge 1,600$ with a performance density $\ge 5.92$), with a policy of “presumption of denial.” That rule also introduced the concept of “Total DRAM Bandwidth,” placing any chip with a bandwidth $\ge 4,100 \text{ GB/s}$ under control.

It is important to note that the latest adjustment includes several new restrictive conditions:

- Supply Certification: Applicants (such as Nvidia and AMD) must prove there is sufficient supply for the U.S. market and that exports to China will not delay orders for U.S. customers or impact global foundry capacity.

- Volume Cap: Exporters must commit that the volume of products exported does not exceed 50% of their total sales within the United States.

- Non-Military Use: The products must not be used for military purposes.

- Third-Party Testing: Every shipment must undergo independent testing at a third-party laboratory located within the United States.

Financial Projections and Strategic Motivation

Market data indicates that Nvidia (NVDA) has reserved 660,000 CoWoS capacity units from TSMC for 2026. If 10% (66,000 wafers) is allocated to the H200—assuming 29 chips per wafer—the total output for the H200 in 2026 is expected to reach 1.9 million units. Under the BIS volume cap, the U.S. and China markets would be allocated approximately 1.266 million and 633,000 units, respectively.

Based on an estimated price of 1.4 million RMB for an 8-GPU module, the H200 could contribute over $47.6 billion in revenue to Nvidia in 2026. Of this, the China market could account for nearly $16 billion—a figure expected to exceed the combined 2025 revenue of all currently listed domestic Chinese AI chip companies.

A key factor in the decision to allow these exports is that the U.S. government will take a 25% revenue share. Based on the projected $16 billion in H200 revenue from China, the U.S. government stands to gain roughly $4 billion from export licenses for this single product alone.

“Inventory Clearing” and Ongoing Restrictions

However, many industry insiders view the BIS move to grant export licenses for the H200 as a way to help Nvidia (NVDA) clear existing inventory. Crucially, the U.S. has not lifted restrictions on the contract manufacturing (foundry) of Chinese AI chips with similar performance and specifications. In other words, the policy allows the sale of products at a certain performance level while continuing to prevent China from manufacturing its own equivalent hardware.

Simultaneously, while the executive branch adjusts regulations to facilitate H200 licenses, the U.S. legislative branch is pushing through another law.

On January 12 local time, the U.S. House of Representatives passed the Remote Access Security Act with a vote of 369 to 22 (39 abstentions). This bill aims to restrict the use of cloud platforms like Google and Amazon to remotely access advanced computing power for training AI models. This move could potentially disrupt the collaborative construction of data centers overseas.

The aforementioned researcher emphasized that if the bill is passed by the Senate and signed into law, such international projects may have to be withdrawn.