As the U.S. stock market enters 2026 trading at elevated valuation levels, Bank of America Securities strategist Savita Subramanian is advising investors to look beyond the aggregate market and focus on selective sector opportunities—specifically Healthcare and Real Estate.

In a strategy report released on December 31 titled “Lifelines Beyond AI,” Subramanian noted that the S&P 500 appears expensive across nearly every major valuation metric, though structural differences make direct historical comparisons not entirely precise.

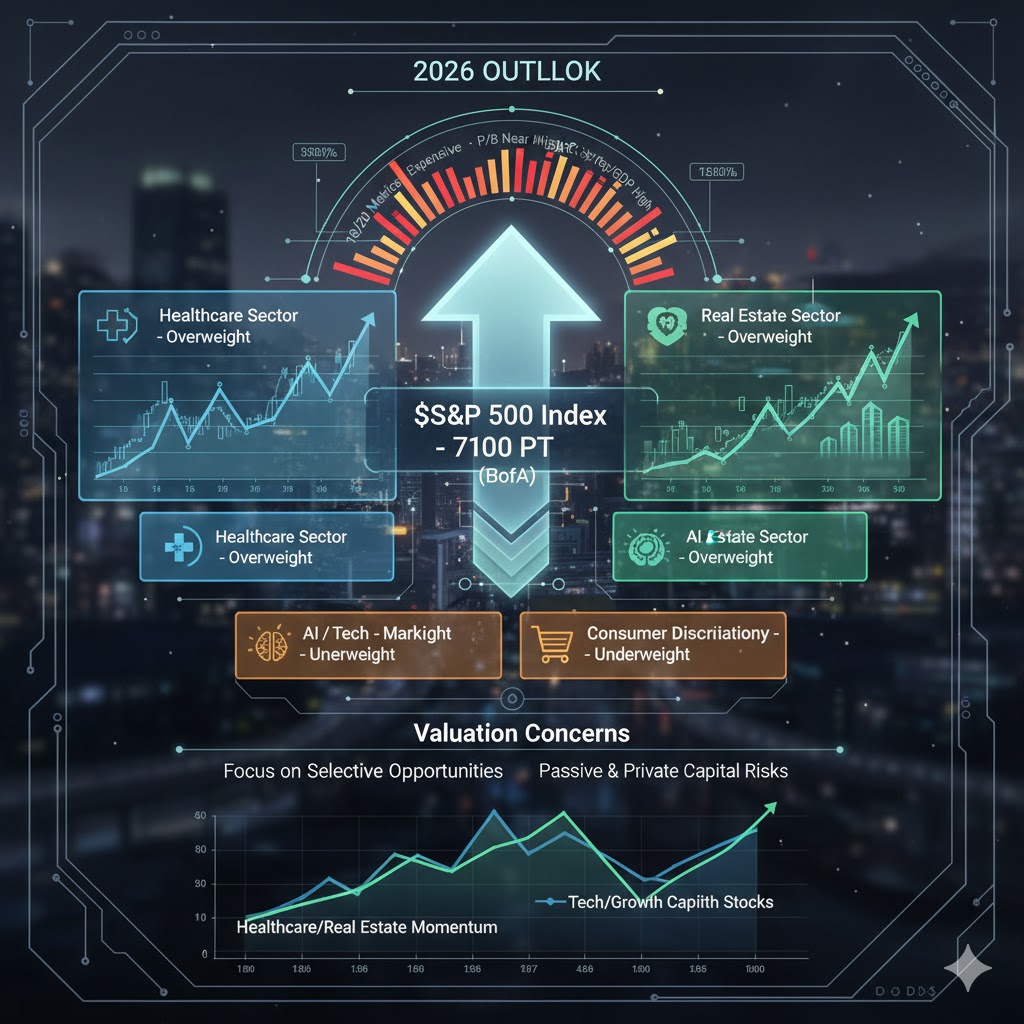

Out of the 20 valuation metrics tracked by the institution, the index shows expensive levels in 18 of them. Key indicators such as Market Cap-to-GDP, Price-to-Book (P/B), Price-to-Operating Cash Flow, and Enterprise Value-to-Sales are all hovering near historical highs. In nine of these metrics, current valuations have already surpassed the levels seen during the peak of the dot-com bubble in March 2000.

While today’s index composition reflects higher-quality, asset-light, and lower-leverage companies compared to previous cycles, Subramanian stated that risk remains high at the index level. Bank of America has set a year-end 2026 target for the S&P 500 at 7,100 points, which is below the general market consensus.

“A bull market always exists somewhere,” the report stated, advocating that investors should focus on industrial sectors rather than simply holding the index.

Healthcare and Real Estate Stand Out

Bank of America’s short-term momentum and valuation models currently rank the Healthcare sector as the most attractive industry, with Real Estate ranking third. For investors with an approximately 12-month horizon, the bank maintains an “Overweight” rating on both sectors in its U.S. equity strategy.

The strategist noted that these two sectors are not only cheap relative to historical market valuations but are also benefiting from upward revisions in earnings estimates and a period of sustained relative outperformance. This combination suggests “true value” rather than just being statistically cheap.

The Tech sector ranked second in the model, but Bank of America maintains a “Market Weight” stance on it, citing increasing uncertainty over how the proliferation of AI will interact with broader economic dynamics in 2026.

AI and the Consumer: A Growing Tension

Subramanian highlighted a potential conflict between the two forces that have driven earnings growth for the $S&P 500 Index (.SPX)$ in recent years: the rise of Artificial Intelligence and the resilience of the U.S. consumer.

Since the 1980s, professional service workers have been the largest contributors to consumption growth. However, recent hiring trends and corporate commentary suggest that AI may reduce the demand for such roles. In turn, if the jobs created by AI do not materialize quickly, it could drag down the consumer-driven economy.

The strategist remarked that it remains unclear what types of new jobs this wave of AI investment will catalyze, prompting the bank to maintain an “Underweight” stance on the Consumer Discretionary and Communication Services sectors.

Passive and Private Capital Heighten Market Risks

Beyond valuation concerns, the report emphasized structural risks stemming from asset allocation trends among U.S. institutional investors. Many pensions and asset owners have leaned toward a “barbell strategy,” simultaneously allocating to passive S&P 500 exposure and private equity or private credit holdings.

Passive funds now account for the vast majority of the S&P 500’s float market capitalization. Subramanian warned that if pressure in the private credit sector persists, or if interest rates fail to return to a “lower for longer” environment, some asset owners might be forced to sell liquid equity positions to manage portfolio valuations.

Whether this pressure manifests gradually or through a sharp wave of forced selling remains uncertain, but the report argues that either scenario reinforces the case for a more selective strategy for U.S. equities in 2026.

Decreased Short-term Appeal for the Staples Sector

Although Bank of America remains strategically Overweight on the Consumer Staples sector, it is currently underperforming in the tactical model. Subramanian described Consumer Staples as a potential “value trap,” noting that its recent cheapness reflects falling prices rather than improving earnings expectations.

By contrast, Healthcare and Real Estate combine attractive valuations with improving fundamentals, making them the preferred areas for investors amidst an expensive market and a changing economic backdrop.