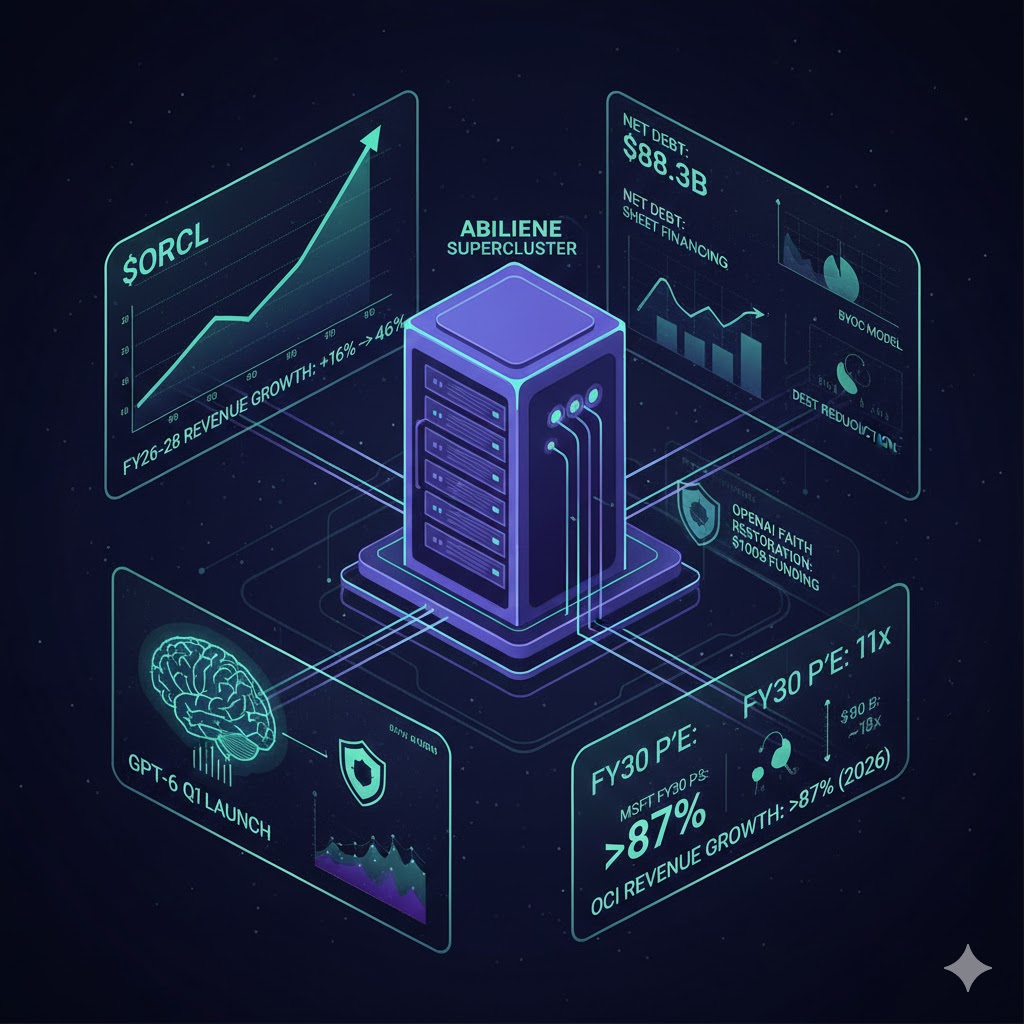

Since its mid-September peak, Oracle’s stock(ORCL) has undergone a severe correction of -41%. This is more than just a technical retracement; it is a direct reflection of crumbling confidence in the “OpenAI Complex.” Investors are currently fraught with anxiety: Can OpenAI deliver on its trillion-dollar promises? Will Oracle’s staggering $88 billion in net debt crush its balance sheet?

According to the latest report from UBS on January 4, the firm offers a distinct contrarian view, reiterating a “Buy” rating. UBS believes the market has over-priced OpenAI’s default risk and Oracle’s financing pressure. If OpenAI completes its new funding round, GPT-6 launches in Q1 as expected, and Oracle utilizes “off-balance sheet” financing to alleviate CAPEX pressure, the market narrative is poised for a fundamental reversal in the first half of 2026.

For investors, Oracle is currently trading at 29x its projected 2026 earnings and only 11x its 2030 projected earnings, offering a highly attractive risk-reward profile.

OpenAI “Faith Restoration”: Funding In-Place and the Redemption of GPT-6

The plunge in Oracle’s share price was not driven entirely by its own operations, but rather by its role as a key “arms dealer” for OpenAI’s computing power. Markets fear OpenAI cannot fulfill its commitments to suppliers. UBS notes that restoring this faith requires only two catalysts: capital and technology.

- Completion of Billion-Dollar Funding: Media reports indicate OpenAI is raising $100 billion at an $830 billion valuation. SoftBank has reportedly fully funded its $40 billion commitment, and Amazon is in talks for a $10 billion investment. Once this capital is secured, the counterparty risk for Oracle vanishes instantly.

- GPT-6 on the Horizon: While ChatGPT user growth is slowing, OpenAI’s CEO has hinted at a major model update (GPT-6) in Q1. If the new model proves that massive compute investment leads to a qualitative leap, it will directly crush competition anxiety from Google’s Gemini and end the “AI bubble” panic.

The Moat Holds: OpenAI Remains the Enterprise King, Gemini Threat Overblown

The release of Google Gemini 3 triggered a “Code Red” crisis within OpenAI and led investors to fear that OpenAI’s growth in the consumer market had peaked. However, UBS’s latest Enterprise AI survey suggests this concern is misplaced in the B2B sector.

- Rising Adoption Rates: Production-grade adoption of Enterprise AI projects rose from 14% in March 2025 to 17% in December. While the pace is steady rather than explosive, the trend is upward.

- OpenAI’s Dominance: Among enterprise users, OpenAI models occupy three of the top five spots (1st, 3rd, and 5th). Despite Gemini’s rising rank, OpenAI remains significantly ahead in terms of enterprise-grade productization.

Debt Black Hole or Financial Engineering? Off-Balance Sheet and BYOC to Save the Balance Sheet

Beyond OpenAI risk, investors are most concerned with Oracle’s own balance sheet. As of the end of the November 2025 quarter, net debt stood at $88.3 billion, with a net debt/EBITDA ratio of 2.8x (potentially reaching 4x under S&P criteria if lease liabilities are included). To maintain its investment-grade rating, Oracle must walk a tightrope between massive CAPEX and debt management.

UBS predicts Oracle’s average annual CAPEX for FY26-FY30 will reach a staggering $72 billion. To bridge the funding gap, Oracle is employing aggressive financing strategies:

- Off-Balance Sheet Financing: By partnering with entities like Crusoe or Vantage to build data centers, Oracle acts only as a tenant, shifting massive infrastructure costs off its balance sheet.

- Bring Your Own Chip (BYOC): Oracle is exploring a model where large customers (like OpenAI) utilize their own direct contracts with NVIDIA to purchase chips and install them in Oracle’s data centers. This would drastically reduce Oracle’s direct capital outlay. UBS estimates that if 50% of capital requirements are solved through such structures, Oracle’s direct financing needs over the next three years could drop from $80 billion to $40 billion, significantly easing credit pressure.

Infrastructure Powerhouse: Abilene Data Center on Track with 100k GB200s Deployed

Rumors of delays at Oracle’s data centers have been rampant, but UBS refutes this through field research and data analysis.

- Incredible Delivery Speed: Oracle disclosed in its earnings call that its “supercluster” in Abilene, Texas, has already delivered over 96,000 NVIDIA GB200 chips as planned.

- Revenue Explosion Imminent: UBS estimates that these 96,000 GPUs contributed only partial revenue in the previous quarter. As capacity ramps up to a peak of 400,000 GPUs, the Abilene project alone could generate $9.5 billion in annualized revenue. UBS expects Oracle Cloud Infrastructure (OCI) revenue growth to accelerate to over 87% in the February/May quarters of 2026.

Valuation Bottom Line: Risks Priced In, A Prime Buying Opportunity?

Despite the uncertainties, Oracle’s growth story remains the most aggressive among tech giants. Company guidance suggests revenue growth will accelerate from 16% to 46% between FY26 and FY28.

UBS conducted a stress test: even in a “disaster scenario” where OpenAI’s revenue contribution drops to zero by FY30, Oracle’s current share price would represent a P/E ratio of only 12.4x for FY30. In the base case, based on the FY30 EPS guidance of $21, the P/E is only 11x. By comparison, Microsoft’s forward P/E is approximately 18x.

UBS argues that the stock’s -36% underperformance (relative to the AI sector average) has over-reflected financing and execution risks. As long as funding lands and infrastructure is delivered as scheduled, Oracle is set for a significant valuation rerating.