On Wednesday (January 7), U.S. defense stocks initially slumped following a rare public rebuke from President Trump during mid-day trading. However, the sector saw a significant rebound during overnight and pre-market sessions, with several companies fully recovering their losses.

Trump’s Criticism of Defense Contractors

Roughly an hour before Wednesday’s closing bell, Trump posted a critique claiming that U.S. defense contractors are issuing massive dividends and conducting large-scale stock buybacks at the expense of investing in plants and equipment. “This situation will no longer be allowed or tolerated!” he wrote.

He accused these firms of being “extremely slow” in delivering critical equipment and failing to provide timely or adequate maintenance. Furthermore, he emphasized that executive compensation packages at these companies are “exorbitant and unjustifiable” given their performance.

Proposed Restrictions and Mandates

Trump demanded that defense companies prioritize building new, modernized production facilities. He outlined several strict conditions to be met until current issues are resolved:

- Executive Pay Cap: Annual compensation for defense executives must not exceed $5 million.

- Payout Ban: A total prohibition on shareholder dividends and stock buybacks.

- Internal Funding: Companies must use existing capital for immediate production rather than seeking government bailouts or loans from financial institutions.

Market Reaction and Financial Data

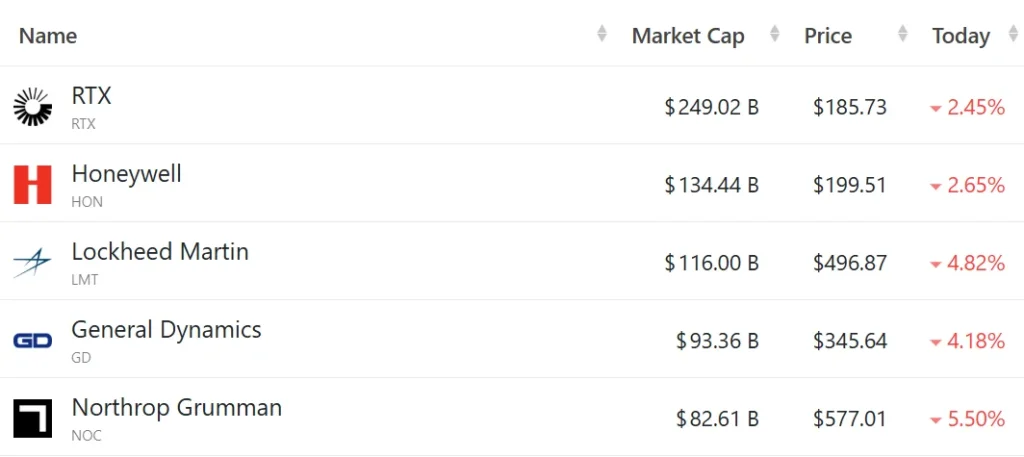

Following the news, defense stocks dropped sharply in late trading. Northrop Grumman (NOC) closed down 5.5%, while Lockheed Martin (LMT) and General Dynamics (GD) fell over 4%. RTX (RTX) declined by approximately 2.5%.

According to financial filings, Northrop Grumman spent $1.17 billion on buybacks and $964 million on dividends in the first nine months of last year. During the same period, Lockheed Martin allocated $2.25 billion for buybacks and $2.33 billion for dividends.

An hour after the close, Trump issued another post specifically targeting RTX. Citing a report from the “Department of War” (Department of Defense), he labeled the company as the “least responsive” and “slowest to expand,” despite being the “most aggressive” in shareholder payouts. RTX, a key supplier for the F-35 fighter jet and advanced missiles, was warned that the Department would cease all business with them unless they increased investments in infrastructure.

The “Deep V” Rebound

The tide turned during overnight trading as defense stocks staged a collective rally. Northrop Grumman and Lockheed Martin rose approximately 6.3%, General Dynamics gained nearly 4.9%, and RTX climbed about 4.8%.

The momentum carried into Thursday’s pre-market session. Northrop Grumman’s gains expanded to nearly 7.3%, Lockheed Martin rose over 6.5%, and RTX increased by 5%.

Analysis: Why the “Ban” is Seen as a Positive

Analysts suggest that Trump’s push to halt dividends can be interpreted as a long-term bullish signal. By redirecting cash into production lines, equipment upgrades, and order fulfillment, contractors could significantly boost their long-term growth potential.

In an era of strained industrial capacity, these policy signals have bolstered investor expectations for future revenue and order growth. Furthermore, Trump proposed on the same day that the FY2027 defense budget be increased from $1 trillion to $1.5 trillion, citing the need for a stronger military in “troubled and dangerous times.”

Industry and Government Perspectives

Palmer Luckey, founder of Anduril Industries—recently valued at $30.5 billion—stated he does not oppose regulatory measures, including pay caps. Luckey noted that he personally “only takes a $100,000 annual salary.”

Additionally, it is worth noting that reports from last August mentioned Commerce Secretary Howard Lutnick hinting that the U.S. government is considering taking equity stakes in the defense industry, similar to its 10% stake in Intel, to ensure better oversight and production.